If you are wondering who pays closing costs in a real estate transaction, both sellers and buyers do. It comes to about 10% to 15% of the total sale price. However, this total is not split equally, as sellers typically pay more due to state laws, concessions, and other factors.

Sellers typically cover around 8% to 10% of the home’s sale price, while buyers shoulder about 2% to 5%. Knowing these costs early gives you the leverage to plan and negotiate, so you aren’t caught off guard at the closing table.

Very often, sellers expect to walk away with the full sale price. But after the closing costs, the actual amount can be surprisingly less. With the listing agent commission being the biggest chunk of the closing costs, you can choose Houzeo to reduce the overall closing costs.

Houzeo is America’s best home buying and selling platform.

For Home Sellers: List your home for a Flat Fee, and save 2.5% to 5.5% on the listing agent commission! That’s thousands of dollars extra in your pocket.

For Home Buyers: Houzeo has the most number of homes for sale in the United States. Start your dream home search now!

👉 Want to know more about us? Watch our “What is Houzeo” video to see the platform in action.

Yes! You can list your home for sale or search millions of homes on the Houzeo mobile app!

Download now on the Apple App Store or the Google Play Store.

Key Takeaways:

- Sellers Pay a Bigger Share: Sellers are expected to cover 8-10% of the sale price in closing costs. That includes Realtor commissions, title fees, transfer tax, and attorney fees.

- Buyers Pay a Smaller Share: Buyers cover about 2%-5% of the sale price as closing costs. That includes lender-related costs like appraisal, loan origination, and recording fees. It’s a smaller portion, but still in thousands.

- Closing Costs Are Negotiable: Keep in mind that who pays what can vary depending on the deal. Seller concessions, for example, are common in real estate transactions and can shift costs between parties.

- Save Big with Smart Choices: Sellers can use a Flat Fee MLS listing service like Houzeo to avoid high commissions. Buyers can negotiate credits or explore assistance programs.

What Are Closing Costs?

Closing costs are essentially the behind-the-scenes expenses that help complete the property ownership transfer from the seller to the buyer. Paid on closing day, they should not be confused with the home’s purchase price and down payment.

The closing costs cover the administrative, legal, and financial work required to complete the sale. For most transactions, these costs range from 10% to 15% of the home’s sale price, depending on whether you are a buyer or a seller.

Yes, the home appraisal cost is typically included in buyer closing costs. Since most lenders require it before approving a mortgage, they hire a licensed appraiser to assess the home’s market value. The cost for the same is paid by the buyer.

That said, unlike most other closing costs, the appraisal fee is paid upfront rather than at the closing table. Nevertheless, it is still generally counted as part of the overall closing costs.

Who Pays Closing Costs: Buyer or Seller?

Sellers and buyers both pay closing costs in a real estate transaction, though their split is not equal. Sellers typically pay 8% to 10% of the sale price, while buyers pay 2% to 5%. That said, the split can vary depending on one’s role in the transaction and negotiation.

In a buyer’s market where inventory is high, or mortgage rates make affordability a challenge, sellers may agree to cover some of the buyer’s closing costs through seller concessions. They do this to attract offers and close the deal faster.

In a seller’s market where demand is high and homes receive multiple offers, buyers may voluntarily cover additional costs. Since sellers have the upper hand, a buyer willing to take on more costs signals seriousness, making their offer harder to pass up.

Yes, closing costs vary depending on the property’s location. For instance, while sellers pay the title insurance premiums in Southern California, the same is customarily paid by the buyer in Northern California.

In New York, transfer taxes are primarily paid by the sellers, but the same is typically split between the buyer and the seller in Washington D.C.

In states like South Carolina, Georgia, and Massachusetts, real estate attorneys are required to be present at closing. Their fees are typically paid by whoever hires them.

What are Seller Concessions?

Seller concessions are costs that the seller agrees to cover toward the buyer’s closing costs. Instead of reducing the home’s sale price, the seller offers credit, reducing the amount the buyer needs to bring to the closing table.

If a seller offers a $6,000 concession on a home priced at $436,523, the buyer still pays the full purchase price. The seller then uses a portion of the proceeds to cover $6,000 of the buyer’s closing costs.

That said, there is a limit to the amount a seller can offer as credits to the buyer based on their loan type and down payment percentage. Here are the different loan types and the maximum concession limit on each of them:

While concessions may seem unappealing for sellers at first glance, there are many benefits to offering them:

- Attracts More Buyers: Many buyers can afford to pay a monthly mortgage but are cash-strapped at closing. By offering a concession, sellers open the door to a larger pool of home buyers.

- Faster Sale: A home sitting on the market for a long time loses its value. Offering a concession can motivate hesitant buyers to commit to the purchase.

- Keeps the Deal Alive: If a buyer is close to backing out due to closing cost concerns, a concession can keep them interested in the deal.

Who Covers Closing Costs in Different Types of Sales?

The general rule states that both sellers and buyers pay the closing costs. However, the exact split varies depending on the type of real estate transaction. A cash sale, a land sale, and a new construction home each come with their own set of fees and expectations.

Who Normally Pays Closing Costs in a Cash Sale?

Both sellers and buyers normally pay closing costs in a cash sale. While sellers pay nearly the same amount as in a traditional sale, the buyer’s closing costs are significantly reduced.

This is because a normal cash sale does not involve a mortgage, allowing buyers to skip all financing-related closing costs. Since only property and paperwork-related costs apply, buyers typically pay around 1% to 3% of the home’s purchase price at closing.

On the other hand, if the cash buyer is an investor or home flipper, they may negotiate for the seller to cover little to no closing costs.

Who Usually Pays Closing Costs on a Land Sale?

Typically, both sellers and buyers pay closing costs on a land sale. While sellers pay similar closing costs to a conventional home sale, buyers may have to bear some additional expenses.

When buying land, buyers pay for land-specific fees such as environmental inspection, land survey, and soil test. These expenses do not apply during a standard home purchase.

Who Generally Pays Closing Costs on a Newly Constructed Home?

Sellers and buyers both pay closing costs on a house that is newly constructed. However, the split differs from a conventional home sale since the seller is typically a builder or developer.

Builders may offer incentives toward closing costs in exchange for using their preferred lender or title company. Buyers, on the other hand, pay costs such as loan origination fees, title insurance, and land closing costs like development fees.

Buyers may also incur some additional expenses related to new construction. These costs typically include the builder’s fees, HOA setup fees, and new construction inspection fees.

Closing costs on a newly constructed home are generally higher than on a resale home. Buyers can expect to pay between 3% and 6% of the purchase price, compared to the usual 2%-5% for existing homes.

For example, on a $350,000 home, new construction carries closing costs of $10,500 to $21,000, compared to $7,000 to $17,500 for an existing home. The difference comes down to additional builder fees, new construction appraisal, and inspections.

How Much are Closing Costs on a Home?

There is no set amount for how much closing costs sellers and buyers pay, but they typically amount to about 10% to 15% of the home’s sale price. However, as a rule of thumb, sellers pay about 8% to 10% of the sale price at closing, while buyers pay about 2% to 5%.

For a home priced at the national average of $436,412, the estimated closing costs for sellers range between $34,912 and $43,641, while buyers pay between $8,728 and $21,820. Unlike sellers, whose closing costs are deducted from their net proceeds, buyers typically pay them out-of-pocket.

Knowing when to expect these costs is equally important. Home buyers typically receive the closing disclosure three days before closing, while sellers receive a net sheet from their agent several times throughout the selling process.

Calculate Your Closing Costs

You do not need to wait for the closing disclosure or net sheet to find out the estimated closing costs on a home. Use the closing costs calculator below to find your closing expenses as a buyer or a seller.

Online closing cost calculators work by taking a few key inputs. You need to enter the home’s sale price, location, and your role in the transaction.

The calculator then applies standard percentage ranges to your purchase price. It then factors in location-specific taxes and fees to produce a breakdown of expected costs. But do keep in mind that the results are estimates and not exact figures.

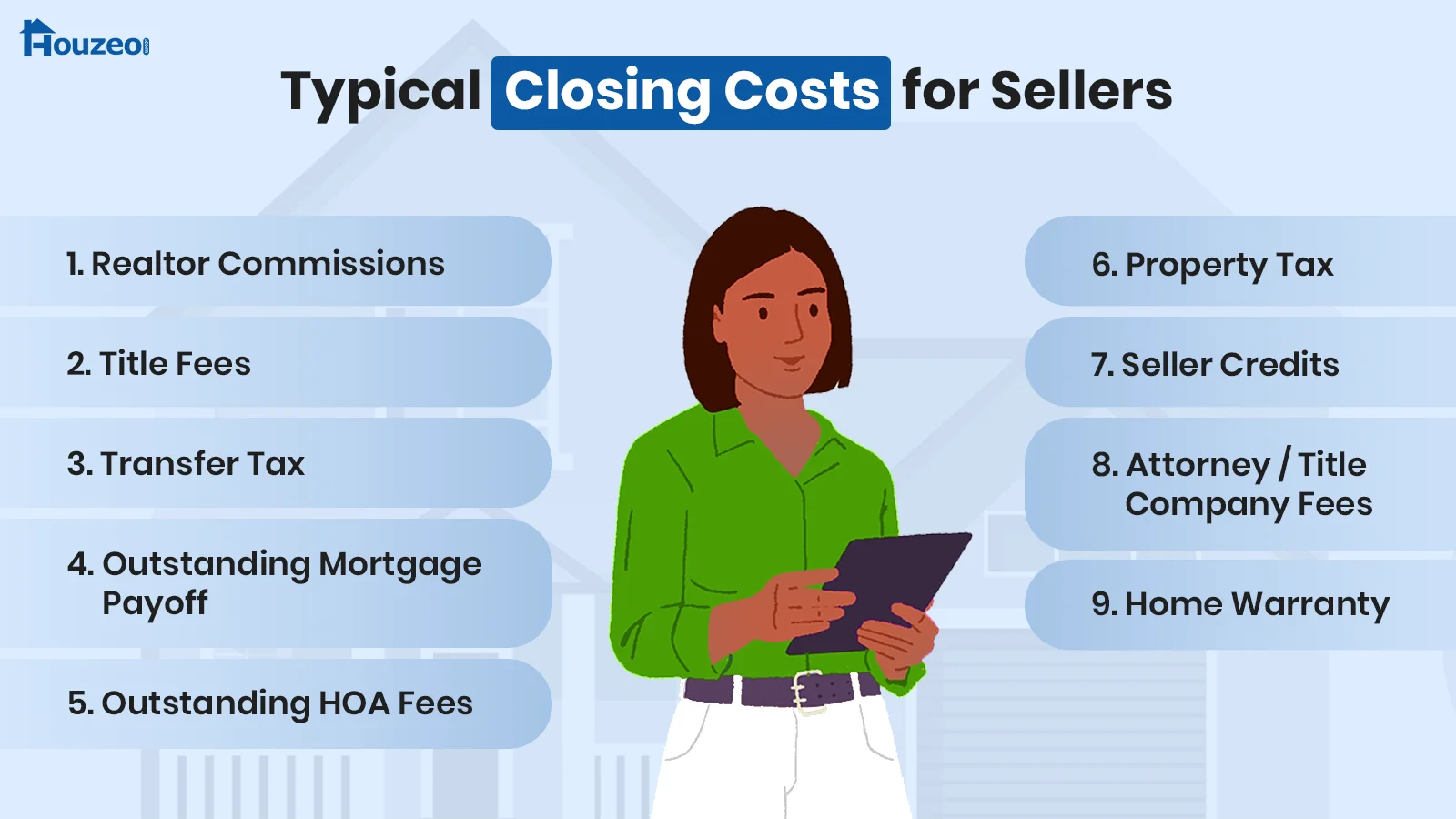

What are Typical Closing Costs for Sellers?

Sellers typically pay costs related to the transfer of property and agent commissions. These costs are directly deducted from the net sale proceeds at closing.

- Realtor Commissions: Realtor commissions are the seller’s biggest closing cost, typically running 5.5%-6% of the sale price to cover both agents. That said, following the 2024 NAR settlement, sellers are no longer required to pay the buyer’s agent commission.

- Title Fees: Title fees cover the cost of verifying and transferring legal ownership, typically including owner’s title insurance and title search. They protect the buyer against title defects and generally range from $1,500 to $5,000+, depending on location and sale price.

- Transfer Tax: Transfer tax is a fee charged by the government when ownership of a property is transferred from the seller to the buyer. The amount varies based on your location and can range from 0.01% to 2% or more of the final sale price.

- Outstanding Mortgage Payoff: If you have an existing mortgage, you must pay off the remaining balance plus any accrued interest at closing. Known as mortgage payoff, this can be one of the largest closing costs for sellers and is typically covered by sale proceeds.

- Outstanding HOA Fees: If your home belongs to a Homeowners Association, any unpaid dues, including monthly or annual fees, must be settled at closing. The HOA will provide a statement outlining the total amount owed, which will appear on your closing disclosure.

- Property Tax: As a seller, you owe property taxes till the day of closing. Since taxes are paid in arrears, the title company will prorate the amount based on the days of ownership and deduct it from your sale proceeds.

- Attorney or Title Company Fees: Whether you hire a real estate attorney or title company to close, expect to pay $500-$1,500 for services like contract review and closing document preparation. The costs vary by location and transaction complexity.

- Seller Credits: Seller credits, or seller concessions, are amounts the seller agrees to pay on the buyer’s behalf at closing. Typically negotiated during the purchase agreement, they help cover the buyer’s closing costs, repairs, or other expenses.

- Home Warranty: A home warranty is an optional perk sellers offer to attract buyers. It covers the repair or replacement of major systems like HVAC, plumbing, and appliances for a set period after closing. They are typically deducted from the seller’s proceeds at closing.

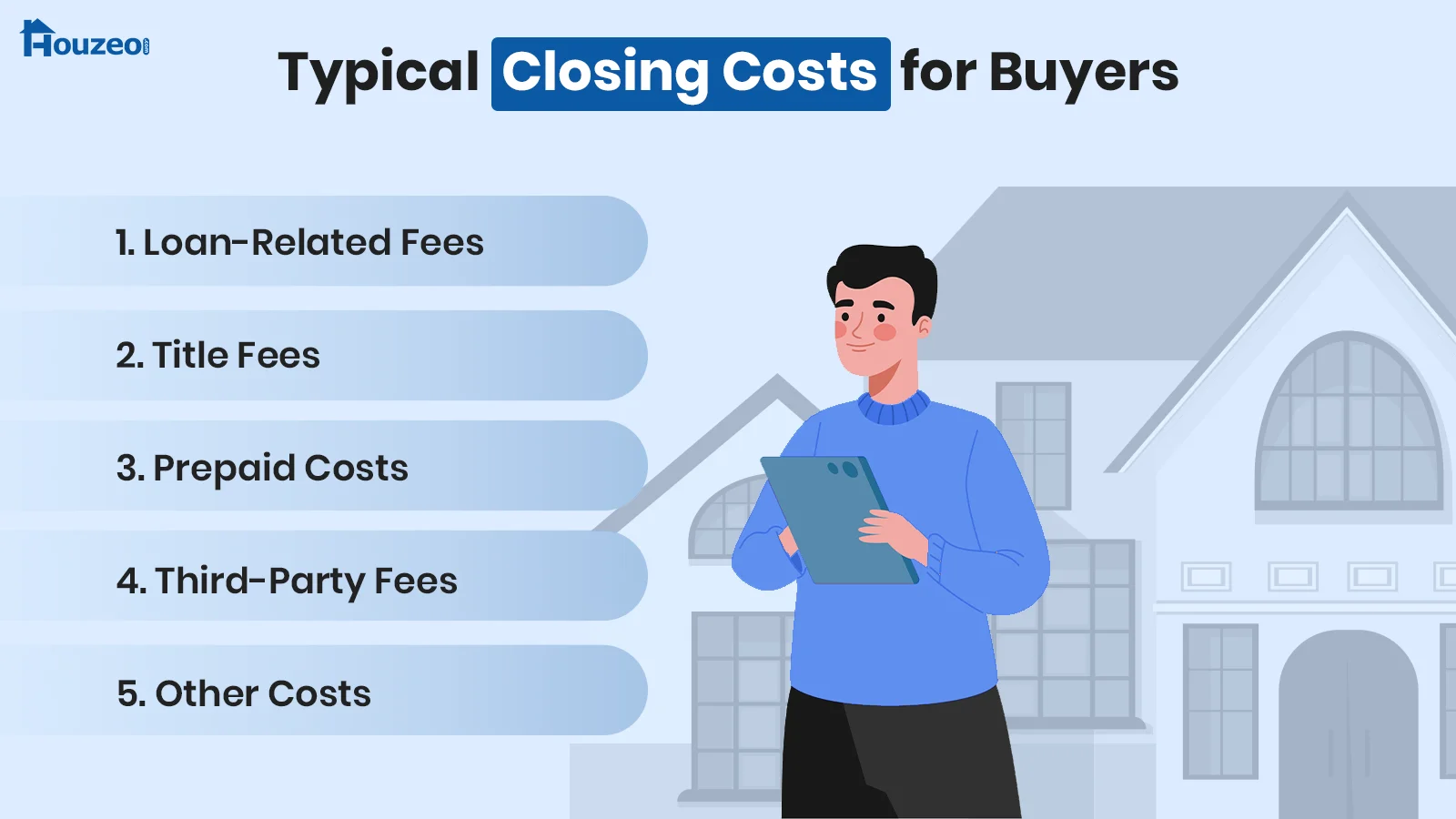

What Are Typical Closing Costs for Buyers?

Buyers typically pay costs related to loan origination and third-party fees like appraisal and home inspection fees. These costs are typically paid out-of-pocket.

1. Loan-Related Fees

Loan-related fees include the money you spend to finance your new home. These include expenses like application fee, loan origination fee, underwriting fee, and discount points.

- Application Fees: When you submit your loan application, the lender collects an application fee. It covers the cost of pulling your credit report and the initial administrative work. Application fees typically range from $200 to $500.

- Loan Origination Fees: The lender charges a loan origination fee to prepare your loan. It covers the administrative tasks like generating loan documents, coordinating with third parties, and processing the loan file. It typically amounts to 0.5% to 1% of the total loan amount.

- Underwriting Fees: The lender charges an underwriting fee to evaluate and verify your loan application. It covers the cost to review your financial documents, credit history, and property details. Underwriting fees typically range from $300 to $900.

- Mortgage Points: At closing, you pay mortgage points directly to the lender to secure a lower interest rate on your mortgage. One point equals 1% of the total loan amount. Buyers pay these to reduce their monthly mortgage payments over the life of the loan.

Yes, you can finance your mortgage closing costs in some cases. Here are your main options:

- Roll Them Into a Loan: Some loan types allow you to add closing costs to your loan. With that, you don’t pay the costs up front, but over the loan’s tenure.

- No-closing cost mortgage or lender credits: The lender covers the closing costs or offers credits towards them in exchange for a higher interest rate.

2. Title Fees

Title fees are charges associated with verifying and transferring ownership of the property. These include title search fees, recording fees, and owner and lender’s title insurances.

- Title Search Fee: A title search fee covers the cost of researching public records to confirm who legally owns the property. This includes looking for any outstanding liens or other claims against it. This service typically costs between $150 and $500.

- Recording Fee: A recording fee is a charge paid to the local government to officially record the transfer of property in public records. The service typically ranges from $50 to $250 and varies between locations.

- Lender’s Title Insurance: Lender’s title insurance is a policy that reimburses the lender if you lose your home to a title claim. The cost is based on the loan amount and typically costs between 0.5% to 1% of the mortgage.

- Owner’s Title Insurance: Owner’s title insurance, similar to the lender’s title insurance, protects the buyer if there is any previously unknown claim on the property. It typically costs 0.5% to 1% of the home’s purchase price.

3. Prepaid Costs

Prepaid costs are upfront payments collected at closing to cover expenses that are due before your first mortgage payment. These include prepaid homeowners’ insurance, property taxes, mortgage interests, and an initial escrow deposit.

- Prepaid Homeowners’ Insurance: Lenders require buyers to prepay the first year of homeowners’ insurance at closing. This ensures the property is insured from the moment ownership is transferred. The cost typically ranges from $1,200 to $2,000.

- Prepaid Property Taxes: Buyers are typically required to prepay a portion of their property taxes upfront. This ensures that funds are available when the tax bill comes due. The amount varies depending on the property’s location, assessed value, etc.

- Prepaid Mortgage Interest: Prepaid mortgage interest is the interest accrued on your property from the closing date to the end of the month. This upfront payment covers the gap between the closing date and the start of the first billing cycle.

- Initial Escrow Deposit: The Initial escrow deposit is the upfront amount collected at closing to fund your escrow account. Your escrow is handled by a third party, who will use the funds to pay for your recurring expenses, such as property taxes and homeowners’ insurance.

4. Third-Party Fees

Third-party fees are charges paid to professionals who provide services that are necessary to complete a home purchase. These include appraisal fees, home-inspection fees, survey fees, and attorney or settlement fees.

- Appraisal Fees: An appraisal fee covers the cost of hiring a licensed appraiser to determine the fair market value of your property. Appraisal fees typically range from $300 to $600.

- Home Inspection Fees: A home inspection fee covers the cost of hiring a licensed inspector to evaluate the physical condition of your property. Home inspection fees typically range from $300 to $500.

- Survey Fees: A survey fee covers the cost of hiring a licensed surveyor to verify the exact dimensions of your property. This ensures that the boundaries are accurate and there are no disputes with neighboring properties. The cost typically ranges from $300 to $700.

- Attorney or Settlement Fees: In some states, you are legally required to hire an attorney for the closing. An attorney or settlement fee covers the cost of coordinating the closing and drawing up paperwork for the title transfer. It typically ranges from $500 to $1,500.

5. Other Costs

Besides loan-related fees, title fees, prepaid costs, and third-party fees, there are some additional costs incurred by a buyer at closing. These include the credit record fee, HOA transfer fee, and Private Mortgage Insurance.

- Credit Report Fee: It is a charge collected by the lender to pull your credit report as part of the mortgage application process. The lender uses the report to evaluate your creditworthiness and eligibility for a loan. The fee typically ranges from $25 to $50.

- Homeowners’ Transfer Fee: If the property you are purchasing is part of a Homeowners Association, you may be required to pay an HOA transfer fees at closing. The fee typically ranges from $100 to $400.

- Private Mortgage Insurance: If you have put down less than 20% of the home’s purchase price, the lender will require you to pay for private mortgage insurance. This protects the lender in case you default on the loan. The cost generally ranges from 0.5% to 1.5% of the loan amount per year.

Some closing costs, like attorney fees and property taxes, are shared between the seller and buyer because both parties have a stake in ensuring a smooth transfer of ownership. The split is often negotiable and is typically agreed upon during purchase contract negotiations.

1. Realtor Commissions

Since sellers are no longer required to pay the buyer agent’s commission, both parties can negotiate to decide how much each will contribute.

2. Attorney Fees

Some states in the U.S. require the involvement of a real estate attorney in processing the transfer of property ownership. Even when an attorney is not required, sellers and buyers can opt for one and share the cost between themselves.

3. Prorated Property Taxes

If taxes are paid in arrears, the seller gives the buyer credits at closing for their share of unpaid taxes. The buyer uses these funds to pay the bill in full when it comes due.

Meanwhile, if the seller has paid the property tax in advance, the buyer reimburses the seller at closing. This amount covers the time the buyer will own the home.

4. Prorated Homeowners Association Fees

Similar to property taxes, HOA fees are also split between the buyer and seller at closing. If the fees are paid in arrears, the seller credits the buyer for their prorated share. If the fees are paid in advance, the buyer reimburses the seller for their time of ownership.

5. Transfer Taxes

Unlike other closing costs, the party responsible for paying transfer taxes vary significantly by state, county, and city.

For instance, in many states like California and New York, the seller pays the transfer tax. In states like Delaware and Nebraska, the buyer bears the cost. Meanwhile, in some states like Pennsylvania, the transfer tax is split between the two parties.

6. Owner’s Title Insurance

Owner’s title insurance costs are typically split between the buyer and seller at closing. The seller pays for the owner’s title policy to deliver a clear title to the buyer. The buyer, on the other hand, may reimburse or share the cost depending on local customs and purchase agreement negotiation.

How to Reduce Closing Costs?

There is no way to waive closing costs completely. However, there are ways through which both sellers and buyers can reduce their closing costs.

How to Reduce Closing Costs for Sellers?

While selling a house, it is only natural that you wish to reduce your closing costs to keep your profits high. To do so, you must identify which fees are negotiable or avoidable.

1. Work With Flat Fee MLS Companies

Real estate commission is the biggest seller closing cost, typically running 5.5%–6% of the sale price. Working with a Flat Fee MLS company like Houzeo lets you avoid nearly half of that. For a small flat fee, your home gets listed on the MLS, saving you the 2.5%-3% listing agent commission.

» Want to know how to list on MLS? Here’s a full guide for you.

2. Sell “For Sale By Owner” (FSBO)

For Sale By Owner (FSBO) means selling your home without an agent, saving you the 2.5%-3% listing agent commission. You can list on free FSBO websites, though they offer limited features and no MLS access. Paid sites provide MLS access, listing syndication, and broader exposure.

3. Research and Compare Services

A real estate transaction often involves hiring several professionals, some of whom may be required by state law. Shopping around and comparing title companies and attorneys can help you find competitive rates and reduce your overall costs.

4. Try to Negotiate Who Pays What

While sellers and buyers each have their own closing costs, some charges are negotiable. In a hot seller’s market where inventory is low, buyers face stiff competition and may willingly cover some of the seller’s costs just to secure the deal.

Time Your Closing Date You can reduce your closing costs as both a seller and a buyer by timing your closing date. For buyers, closing near the end of the month reduces the amount of prepaid interest owed at closing. For sellers, timing the closing right can help avoid an extra month of carrying costs such as mortgage interest, HOA fees, and property taxes.

How to Reduce Closing Costs for Buyers?

While buying a house, it is only natural that you want to reduce your closing costs to keep your expenses low. To do so, you must identify which fees are negotiable or avoidable. Here are the most effective ways to reduce closing costs as a buyer:

1. Ask for Seller Concessions

While it may seem unlikely for sellers to agree to concessions, it is possible in a buyer’s market. When inventory is high and buyer demand is low, sellers may offer concessions to motivate buyers to purchase their home.

2. Research Closing Costs Assistance Programs

Several state and local government programs offer grants and assistance to help buyers cover their closing costs, particularly for government-backed loans like FHA, VA, and USDA loans. First-time buyers are often the primary beneficiaries of such financial assistance.

However, the eligibility criteria vary by program, location, and loan type. So, it is important to research your options early and identify what programs you can qualify for.

3. Shop for Mortgage Lenders

Research different mortgage lenders and compare their rates before committing to one. Reviewing Loan Estimates can help you identify the lowest origination fees, potentially saving you thousands of dollars.

You can also consider a no-closing-cost mortgage. Such lenders cover your closing costs in exchange for a higher interest rate.

4. Ask About Waiving or Reducing Fees

Many buyers do not realize that you have the ability to push back on certain lender charges. Charges such as application fees and courier fees can sometimes be waived or reduced by simply asking your lender.

While not all lenders may agree to waive the fees, having a strong credit profile can give you leverage to negotiate. You can also get quotes from multiple lenders to give you a stronger position during negotiation.

Look for Closing Disclosure Errors You can reduce your closing costs as both a seller and a buyer by reviewing your Closing Disclosure for errors, which are more common than you might think. Even a small mistake can cost you thousands of dollars.

Who Pays Closing Fees Near Me

| Region | Closing Costs for Sellers |

|---|---|

| Northeast | Connecticut | New Hampshire | New Jersey | New York | Pennsylvania | Rhode Island | Vermont | Delaware | Maine |

| Midwest | Illinois | Indiana | Iowa | Kansas | Michigan | Minnesota | Missouri | Nebraska | North Dakota | Ohio | South Dakota | Wisconsin |

| South | Alabama | Arkansas | Florida | Georgia | Kentucky | Louisiana | Maryland | Mississippi | North Carolina | Oklahoma | South Carolina | Tennessee | Virginia | Texas | Washington, D.C. | West Virginia |

| West | Alaska | Arizona | California | Colorado | Hawaii | Idaho | Montana | Nevada | New Mexico | Oregon | Utah | Washington | Wyoming |

Plan Ahead and Save on Closing Costs

You have to budget for closing costs irrespective of whether you are a home seller or a buyer. In most transactions, sellers and buyers both pay their parts, but it’s common to negotiate closing costs.

Home buyers can ask for seller concessions, negotiate with lenders, or opt for a no-closing-costs mortgage to save on expenses. On the other hand, sellers should discover ways to reduce real estate commissions, which form the biggest chunk of their closing costs.

With Houzeo, sellers can save thousands in commissions. Houzeo gets your property listed on the MLS and equips you with the tools needed to manage the selling process without a real estate agent.

» Houzeo Reviews: Find out what customers have to say about Houzeo – America’s best home selling and buying website.